The UK rental market has entered a period of unprecedented regional divergence as of March 2026, with the North East of England recording the fastest price acceleration in the country while the London market hits a definitive affordability ceiling.

Data released this Monday confirms that the traditional north-south divide in housing economics is being rewritten by a squeeze on supply in northern hubs and a cooling of demand in the capital. While London remains the most expensive place to live in the British Isles, the pace of its growth has been eclipsed by northern regions where available stock has reached historic lows.

Independent news UK analysis suggests that the current trajectory is creating a two-speed rental economy, where "untold stories" of displacement are becoming common in regions previously considered affordable. For many households, the gap between wage increases and rental hikes is narrowing to a breaking point, despite a national slowdown in inflation.

The figures highlight a significant shift in the British property landscape, driven by high interest rates, a reduction in the number of private landlords, and a changing employment market that no longer prioritises central London residency to the same degree as the previous decade.

The North East Paradox: Fastest Growth on Lowest Base

The North East of England has emerged as the epicentre of the UK’s rental inflation, recording an annual growth rate of 7.6%. This figure represents the highest surge in the country, a startling statistic for a region that historically offered the most competitive housing costs in mainland Britain.

Average monthly rents in the North East now sit at approximately £770. While this remains significantly lower than the national average, the velocity of the increase has caught local authorities and tenants off guard. The rapid rise is attributed to a chronic shortage of available properties as buy-to-let investors exit the market in response to tighter regulations and higher borrowing costs.

In cities such as Newcastle, Sunderland, and Middlesbrough, the competition for a single rental listing has increased by 40% over the last twelve months. Estate agents report that properties are often let within hours of appearing online, frequently following bidding wars that drive the final price well above the initial asking figure.

This paradox: of having the lowest absolute rents but the highest percentage growth: places a unique strain on the local economy. Wages in the North East have not kept pace with a 7.6% jump in housing costs, meaning that real-term disposable income for renters in the region is retracting faster than in almost any other part of the United Kingdom.

Industry analysts suggest that the North East is currently experiencing a "catch-up" effect. For years, the region lagged behind the rest of the country in terms of property value growth, but the current lack of new social housing and the stagnation of the private build-to-rent sector have created a perfect storm of high demand and zero elasticity in supply.

For many residents, the "untold stories" of this crisis involve young professionals and families being priced out of their home towns. The transition from a low-cost rental haven to a high-growth pressure zone is occurring without the corresponding infrastructure or salary increases seen in the south of England.

London’s Cooling Market and the Affordability Ceiling

In stark contrast to the volatility in the North, London’s rental market has entered a cooling phase following a peak in autumn 2025. Annual rent growth in the capital has slowed to between 1.7% and 2.0%, the lowest rate of increase across all English regions.

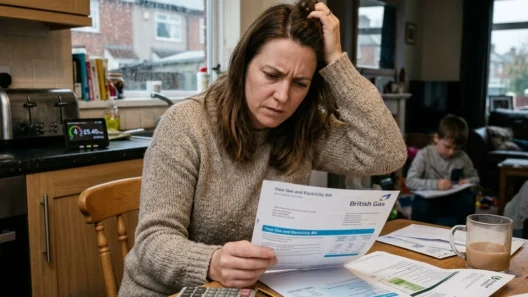

This deceleration marks four consecutive months of decline in the rate of growth, suggesting that the capital has finally hit an affordability ceiling. With average monthly rents still hovering between £2,067 and £2,273, the market has reached a point where the vast majority of the workforce simply cannot sustain further increases.

Tenants in London currently spend an average of 38.3% of their gross income on rent, compared to a national average of 32.4%. This high burden has triggered a shift in tenant behaviour. Rather than the frenzied decision-making seen in 2024 and 2025, London renters are now taking longer to commit to tenancies, showing less urgency and negotiating more aggressively on price.

The "cooling" of the London market is relative, however. While the rate of growth is slow, the absolute cost remains a significant barrier to entry for many. The slowdown is largely driven by a limit on what the market can bear; as rents consume nearly 40% of income, there is little room for landlords to push prices higher without facing prolonged vacancies.

Furthermore, the prestige of a London postcode appears to be waning for certain demographics. The rise of hybrid working models and the improved digital infrastructure in satellite towns have allowed workers to look beyond the M25, further dampening the demand that previously fuelled double-digit growth in the city's central zones.

Despite the slowdown, the supply of rental stock in London remains constrained. The cooling growth rate is not a result of a sudden influx of new homes, but rather a correction where demand has finally been stifled by the sheer weight of the cost of living. For the average Londoner, a 1.7% increase on a £2,000 rent is still a substantial monthly outgoing in a period of high utility and food costs.

National Implications of a Fractured Housing Sector

The divergence between the North East and London reflects a broader, national housing crisis that continues to outpace policy interventions. Across the UK, rents increased by an average of 3.5% annually through February 2026, while wage growth sat at approximately 3.8%.

On paper, wages are marginally outperforming rents at a national level. However, this macro-level data masks the regional reality where, in areas like the North East, the cost of shelter is rising twice as fast as the money coming into households. The national average is skewed by the stagnation in London and the South East, hiding the acute pressure felt in the Midlands and the North.

The UK economy remains braced for the long-term impact of this rental volatility. High housing costs are a primary driver of labour immobility; workers are increasingly unable to move to areas where their skills are needed because they cannot find affordable accommodation. This has a direct correlation with the national productivity gap and the ongoing struggle to stimulate growth in post-industrial regions.

Government data indicates that the number of households in the private rented sector has remained static, yet the composition of landlords is changing. Small-scale landlords are being replaced by institutional "Build to Rent" developers. While this brings a more professional management style to the sector, these developments are often targeted at the higher end of the market, leaving a vacuum for low-to-middle income earners.

The "untold stories" of 2026 involve a growing demographic of "perpetual renters": individuals in their 40s and 50s who have no prospect of entering the property ladder and are now facing the highest rental volatility in the developed world. The lack of security in the private sector, combined with regional price spikes, has made housing the primary concern for voters across the political spectrum.

As the second quarter of 2026 approaches, the outlook for the rental market remains uncertain. While London may continue to see a plateau in prices, the pressure on the North East and similar regions is expected to persist until a significant increase in social and affordable housing stock is realised. The rental crisis is no longer a London-centric issue; it is a nationwide challenge with deeply regional consequences.