Millions of UK households are facing a significant financial squeeze as the 2026 broadband price hike cycle takes full effect across the country. New analysis suggests the cumulative impact of these mid-contract increases will drain an estimated £6.85 billion from the British economy over the coming period, leaving families to navigate a digital landscape that is becoming increasingly unaffordable. While individual monthly increases may appear modest, the aggregate figures tell a different story of a sector prioritising revenue protection over consumer stability.

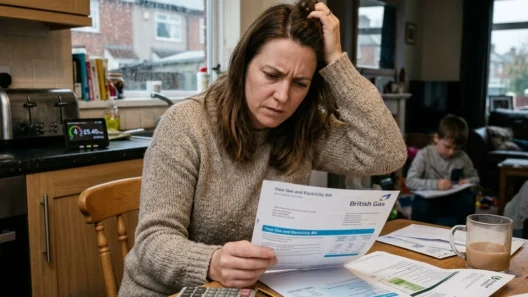

The hikes, which typically trigger in March or April each year, have seen some providers increase monthly premiums by as much as 11 per cent. This figure is more than triple the current rate of inflation, sparking fresh debate over the fairness of mid-contract price adjustments. Independent news UK reports indicate that the average monthly broadband bill now sits at approximately £35.90, but for many, the latest adjustments will add between £36 and £48 to their annual household expenditure. For those on the tightest budgets, this shift is not merely a statistical fluctuation but a genuine threat to their ability to remain connected to essential services.

Industry experts point to the £6.85 billion figure as a combination of direct consumer costs and the long-term inflationary pressure exerted by the telecommunications sector. As broadband is now classified as a utility equivalent to water or electricity, the lack of flexibility in switching providers mid-contract has left millions of users in a "loyalty trap." Untold stories of digital exclusion are beginning to emerge from rural and low-income urban areas where the choice of provider is limited and the cost of exit fees remains prohibitively high.

The structural mechanics of the 2026 price surge

The primary driver behind this multi-billion pound shift lies in the contractual framework used by major telecommunications firms. Historically, providers have utilised a formula of the Consumer Price Index (CPI) or Retail Price Index (RPI) plus an additional percentage, often 3.9 per cent. In 2026, while wider economic inflation has begun to stabilise, the "plus" element of these contracts continues to drive prices upward at a rate that outstrips wage growth. This mechanism ensures that even during periods of low inflation, the cost of connectivity remains on a permanent upward trajectory.

Ofcom, the industry regulator, has previously scrutinised these practices, leading to a shift towards "pounds and pence" price rises. However, the 2026 data suggests that this change has done little to blunt the financial impact on the end-user. Whether expressed as a percentage or a flat fee, the result remains the same: a steady extraction of capital from households. Market leaders including BT, Virgin Media O2, and TalkTalk have all implemented various versions of these increases, citing the need for continued investment in the UK’s fibre-optic infrastructure as the primary justification for the additional costs.

The £6.85 billion truth also encompasses the hidden costs of these hikes. Businesses, particularly small to medium enterprises (SMEs) that rely on high-speed internet for daily operations, are seeing their overheads climb. Unlike residential customers, many business contracts offer even fewer protections against mid-term adjustments. The cumulative effect across the commercial sector contributes significantly to the multi-billion pound total, potentially slowing digital transformation projects and reducing the competitive edge of UK-based startups. The ripple effect of higher communication costs is felt throughout the supply chain, as businesses often pass these costs onto their own customers.

Economic implications for UK households and the digital divide

The distribution of this financial burden is notably uneven. Lower-income households, which spend a higher proportion of their disposable income on utilities, are being hit hardest by the £6.85 billion total cost. While social tariffs exist, uptake remains stubbornly low, with many eligible customers unaware that cheaper options are available. This has led to a widening digital divide, where access to high-speed internet is increasingly becoming a tiered luxury rather than a universal right. Independent news UK analysis suggests that without intervention, up to 15 per cent of the population could face "digital poverty" by the end of the decade.

The untold stories of those affected include elderly citizens who rely on the internet for telehealth services and families with children who require connectivity for educational purposes. For these groups, a £4 monthly increase is not a minor inconvenience; it is a forced trade-off against other essentials like heating or groceries. The psychological impact of "bill shock" is also a growing concern for mental health advocates, as the predictability of household expenses is eroded by complex contractual terms that many consumers struggle to decipher at the point of purchase.

Furthermore, the regional impact of these hikes varies. In areas where infrastructure competition is high: primarily major cities like London, Manchester, and Birmingham: some consumers can find better deals to offset the hikes. However, in "alt-net" deserts where only one major provider offers high-speed services, residents have no choice but to absorb the costs. This geographic disparity means that the £6.85 billion burden is disproportionately carried by those in less connected regions, further entrenching the economic gaps between the North and South of England. The lack of a unified national pricing strategy means that your postcode can determine your level of financial exposure to the 2026 hikes.

Industry justification versus the consumer reality in Britain

Telecommunications giants argue that the revenue generated by these increases is vital for the roll-out of 5G and full-fibre broadband across the United Kingdom. They point to the rising costs of energy, labour, and hardware required to maintain and expand the national grid. According to industry spokespeople, the £6.85 billion figure represents an investment in the country’s future, ensuring that the UK remains a leading digital economy. They maintain that without these predictable revenue streams, the pace of infrastructure deployment would stall, leaving Britain behind its European and global counterparts.

However, critics and consumer advocacy groups challenge this narrative. They point to the significant profit margins and dividend payments of the leading firms, suggesting that the cost of infrastructure investment could be absorbed by corporate balance sheets rather than being passed directly to the consumer. The debate has reached the corridors of Westminster, with some MPs calling for a total ban on mid-contract price rises. They argue that the price agreed upon at the start of a 24-month contract should remain fixed, providing consumers with the certainty they need to manage their finances.

As the 2026 cycle continues to roll out, the pressure on both the government and the regulator to act is mounting. The £6.85 billion truth serves as a stark reminder of the scale of the issue. While the transition to a more digital-centric society is inevitable, the question of who pays for that transition: and at what cost to the average citizen: remains unanswered. For now, millions of Britons will see their bank balances dwindle as the price of staying online continues to rise, marking 2026 as a pivotal and challenging year for the UK’s telecommunications market. The long-term consequences for consumer trust and market stability are yet to be fully realised, as the nation grapples with the high price of connectivity.