The Organisation for Economic Co-operation and Development (OECD) has issued a sobering update regarding the United Kingdom’s economic trajectory. In its latest report, the international body suggests that the UK is facing a period of significantly dampened growth. While the global economy has shown pockets of resilience over the last year, the UK remains particularly exposed to the tremors of geopolitical instability.

Current projections indicate that the UK economy will struggle to maintain the momentum seen in the earlier parts of the decade. The primary drivers behind this cooling effect are rooted in the ongoing volatility within the Middle East and a broader landscape of international tension. For a nation heavily integrated into global trade and energy markets, these external shocks carry a disproportionate weight.

Economic analysts at the OECD have pointed out that the UK's recovery is now "losing steam." The combination of high interest rates and fluctuating energy prices has created a difficult environment for both businesses and households. As the geopolitical situation shifts, the certainty required for long-term investment appears to be evaporating, leaving the British economy in a precarious position as we move further into 2026.

The Geopolitical Ripple Effect on Energy and Trade

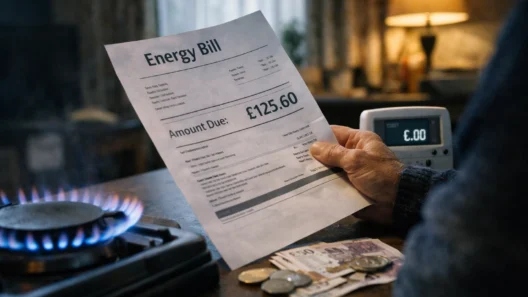

The most immediate concern highlighted by the OECD is the direct impact of Middle Eastern conflicts on global energy supply chains. For the UK, which has been striving to decouple itself from volatile fossil fuel markets through green initiatives, the transition period remains a point of vulnerability. When tensions rise in oil and gas producing regions, the wholesale price of energy spikes almost instantly on the international stage.

These spikes do not just affect the cost of heating a home or filling a car. They filter through the entire economy. Manufacturing sectors that rely on high energy inputs find their margins squeezed, often leading to reduced output or increased prices for the consumer. The OECD suggests that these "second-round effects" are a major contributor to the slowing growth rates observed in the first quarter of this year.

Beyond energy, the disruption of key shipping routes has added another layer of complexity. Increased insurance premiums for cargo vessels and the necessity of taking longer, more expensive routes around the Cape of Good Hope have driven up the cost of imported goods. For a country like the UK, which imports a vast majority of its consumer electronics, clothing, and out-of-season produce, these logistics costs act as a hidden tax on growth. The OECD report warns that if these disruptions persist, the UK could see a prolonged period of sluggish industrial activity.

Domestic Pressures and the Inflationary Tug-of-War

While external factors are the primary focus of the OECD’s warning, the domestic landscape in the UK is not without its own challenges. The Bank of England has been locked in a difficult battle with inflation for several years. Although figures had begun to stabilise, the new wave of geopolitical uncertainty threatens to push inflation back above the target of 2%. This leaves policymakers in a difficult "tug-of-war" scenario.

If the Bank of England maintains high interest rates to combat the rising costs of imports and energy, it risks stifling domestic spending. High borrowing costs have already cooled the housing market and reduced the amount of disposable income available to the average British family. On the other hand, cutting rates too early could allow inflation to embed itself further into the economy, leading to a devalued currency and even higher costs for imported essentials.

The OECD notes that business confidence in the UK has taken a noticeable hit. Small and medium-sized enterprises (SMEs) are particularly wary of taking on new debt or expanding their workforces while the global outlook remains so clouded. This hesitancy to invest is perhaps the most damaging aspect of the current slowdown. Without capital investment, productivity remains stagnant, and without productivity gains, the long-term growth potential of the UK economy is severely limited.

The labour market also shows signs of cooling. While unemployment remains relatively low by historical standards, the pace of wage growth is starting to lag behind the cost of living once again. This creates a feedback loop where reduced consumer demand leads to lower business revenues, which in turn leads to a more cautious approach to hiring and pay increases. The OECD suggests that the UK government must find a way to break this cycle by fostering an environment that encourages domestic stability despite the chaos abroad.

Strategic Recommendations for Economic Resilience

In response to these challenges, the OECD has outlined several strategic recommendations aimed at bolstering the UK’s economic resilience. The overarching theme is the need for diversification and a more aggressive pursuit of energy independence. By accelerating the shift towards domestic renewable energy sources, the UK can shield itself from the price shocks associated with Middle Eastern instability.

Furthermore, the OECD emphasizes the importance of strengthening trade ties with a broader range of international partners. Reducing reliance on a few specific corridors or suppliers can help mitigate the impact of localised geopolitical conflicts. This involves not only formal trade agreements but also investing in the infrastructure required to handle a more diverse array of imports and exports.

Education and skills training also feature heavily in the report. The OECD suggests that for the UK to remain competitive in a slowing global market, it must ensure its workforce is equipped for the digital and green economies. By addressing the long-standing skills gap, the UK can drive productivity from the bottom up, providing a buffer against external economic downturns.

There is also a call for fiscal prudence. The OECD warns that while government intervention may be necessary to support the most vulnerable during energy price spikes, such measures must be targeted and temporary. Maintaining a sustainable fiscal position is crucial for retaining the confidence of international markets, especially when the global economic climate is so uncertain. The report concludes that while the path ahead is difficult, a focus on structural reforms and domestic stability could see the UK emerge from this period of slow growth with a more robust and adaptable economy.

As the government considers its next steps, the weight of the OECD’s warning is clear. The era of "cheap" global trade and stable energy is, at least for now, a thing of the past. Adapting to this new reality is the primary challenge for the UK's economic architects in 2026. The focus must now shift from simply managing the current crisis to building a foundation that can withstand the next one.

The slowdown in growth is not an inevitability of the future, but a reflection of the current global friction. How the UK chooses to navigate these geopolitical waters will determine its economic standing for the remainder of the decade. Stability, it seems, is no longer something that can be taken for granted; it is something that must be actively built through careful policy and strategic international engagement.