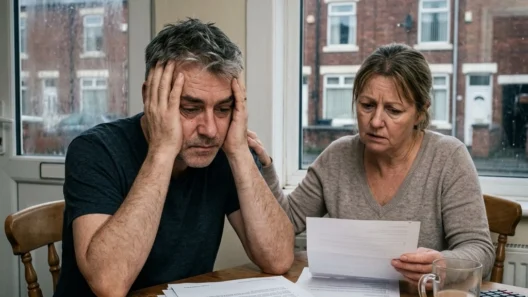

For a long time, the deal was simple. You go to university, you work hard, you get a degree, and you step into a career that pays enough to make the effort worthwhile. It was the standard route to social mobility in the UK. But for a huge portion of the British middle class, that deal is starting to feel more like a trap. We are looking at a generation that is not just starting their adult lives with a bit of debt, but is effectively tethered to a financial weight that dictates where they live, how they work, and if they can ever truly afford to settle down.

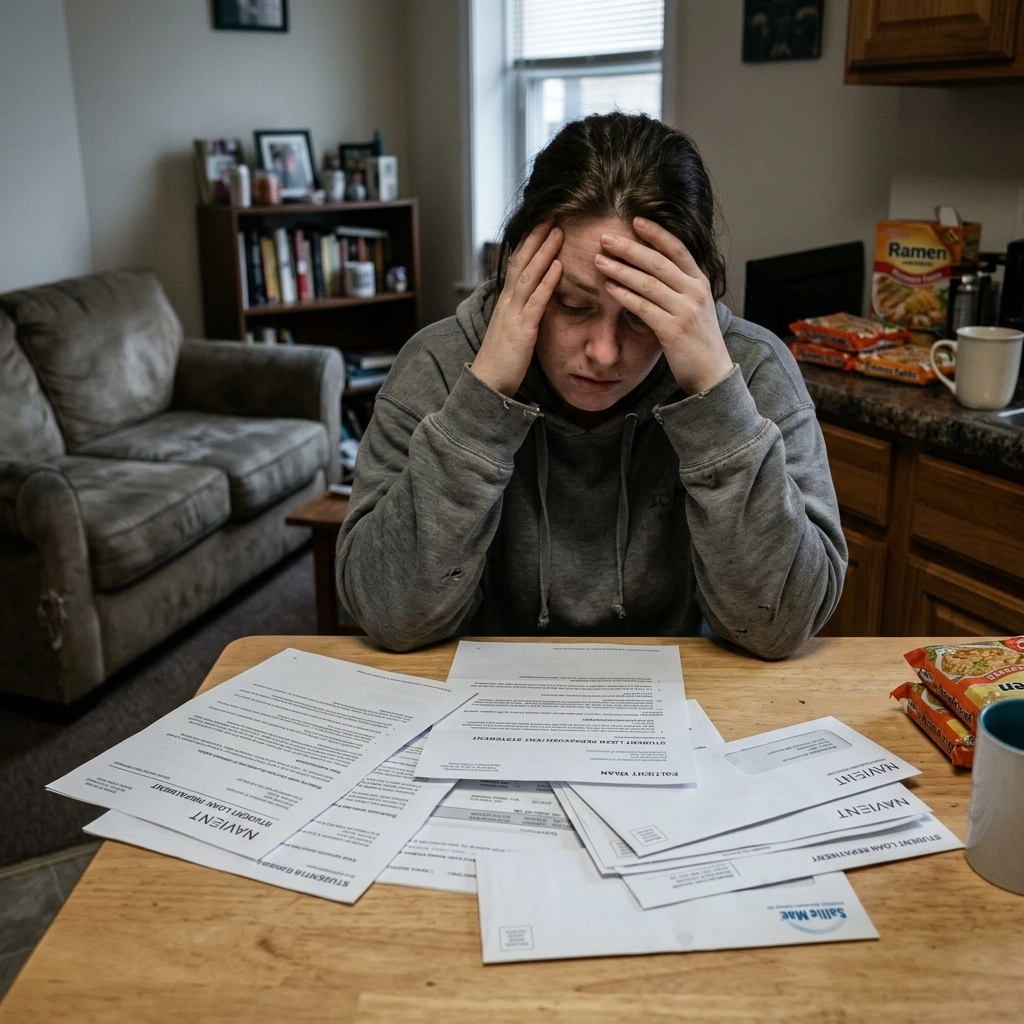

When we talk about the student loan crisis, the conversation often gets bogged down in political jargon or abstract figures. We hear about "billions of pounds in outstanding debt" or "interest rate adjustments," but we rarely talk about the human cost. This is one of those untold stories that independent news UK outlets are finally beginning to peel back. It isn't just about the money leaving a bank account every month; it is about the quiet erosion of the middle-class dream.

In the UK, the student loan system has shifted from a supportive grant-based model to a high-interest loan structure that functions more like a lifelong graduate tax. For many, the balance doesn't just sit there; it grows. Even as professionals work fifty-hour weeks and climb the corporate ladder, they often find their debt increasing rather than decreasing because of how interest is applied. It is a cycle that feels impossible to break, and it is having a profound impact on the psychological and financial health of the country.

The Stealth Tax on Ambition and Growth

The current student loan system in the UK is essentially a stealth tax on the very people the economy relies on for growth. For those on Plan 2 or the newer Plan 5 loans, the interest rates can be eye-watering. Unlike a mortgage or a standard bank loan, where the interest is usually tied to a stable base rate, student loan interest often fluctuates with the Retail Price Index (RPI). When inflation spikes, the interest on these loans goes through the roof.

For a young professional earning a decent salary, a significant chunk of their monthly income is sliced off before it even hits their bank account. This wouldn't be so bad if it were actually clearing the debt. However, because the interest rates have been so high: sometimes reaching double digits: many graduates find that their monthly repayments don't even cover the interest being added to the pile. They are essentially running on a treadmill that is moving faster than they can keep up with.

This creates a bizarre situation where a mid-level manager or a specialist nurse might see their total debt increase every single year, despite never missing a payment. It is a demoralising reality that shapes how people view their future. It is not just a financial burden; it is a psychological one. Knowing that a portion of your hard work is being siphoned off indefinitely to pay for a degree that is supposedly the "key to success" creates a sense of resentment and exhaustion. This is the kind of reality that often goes ignored, making it one of the most pressing untold stories of our time and a clear issue for independent news uk to keep examining.

Why the Middle Class is Feeling the Squeeze

The UK middle class is often referred to as the "squeezed middle," and student loans are a primary reason why. While those from the wealthiest backgrounds can often pay tuition fees upfront to avoid interest, and those on the lowest incomes may have more of their debt written off eventually, the middle-income earners are stuck in the middle. They earn enough to make substantial repayments, but not enough to clear the balance before the interest compounds out of control.

This has a massive knock-on effect on the wider economy. Think about the traditional milestones of adulthood: buying a first home, starting a family, or perhaps launching a small business. All of these require capital and a clean credit profile. While student loans don't technically appear on a credit report in the same way a credit card does, they are absolutely factored into mortgage affordability assessments. When a bank looks at how much you can afford to borrow, that £200 or £300 a month going toward student loans is viewed as a committed outgoing.

For many, this is the difference between being able to afford a home in a safe area or being stuck in the rental market indefinitely. We see this play out in cities across the UK, where professionals are priced out of the very communities they serve. The underlying theme is simple: a system that is failing to provide a stable foundation for the people living within it.

The student loan trap also discourages risk-taking. If you know you have a guaranteed monthly deduction from your salary for the next thirty years, you are less likely to quit your stable job to start a company or pursue a creative passion. This stifles innovation and keeps people locked into "safe" corporate roles just to keep their heads above water. The debt isn't just draining bank accounts; it's draining the nation’s entrepreneurial spirit.

The Need for a Transparent and Fair System

If we are going to fix this, we need to move beyond the current "sticking plaster" approach to education funding. The conversation needs to shift towards genuine reform that prioritises the long-term health of the economy over short-term government accounting gains. Independent news uk has a role to play here by highlighting the discrepancies in how these loans are managed and the lack of transparency around interest rate hikes.

There is a growing call for a cap on interest rates to ensure they never exceed a reasonable level, regardless of inflation. Others suggest a total overhaul of the funding model, perhaps moving toward a genuine graduate tax that is more equitable and doesn't allow interest to compound into astronomical figures. The goal should be a system where education is seen as a public good and an investment in the future, rather than a profit-making scheme for the Treasury.

Without reform, we risk creating a permanent underclass of highly educated but financially squeezed individuals. The social contract is being tested. If young people feel that the path to success is actually a path to permanent debt, they will stop engaging with that path. We are already seeing a shift in how people view university, with more looking towards apprenticeships or immediate entry into the workforce to avoid the "debt trap". While vocational training is valuable, it should not become the default simply because the alternative feels financially punishing.

The student loan crisis is a slow-burning problem for the UK middle class. It is a drain on resources, a barrier to home ownership, and a source of constant anxiety for millions. By bringing these untold stories to light, we can start to demand a system that actually rewards hard work and education rather than punishing it with high-interest penalties. It is time to rethink the debt trap and find a fairer way forward.

The current trajectory of student debt suggests that without significant intervention, the economic gap between those with generational wealth and those relying on their own earnings will only widen. Education should be the great equaliser, not a mechanism for long-term financial extraction. As we look toward the future of the UK economy, addressing the student loan burden must be a priority for anyone interested in true social mobility and economic fairness.